A Surprisingly Useful Toaster Lesson

I recently bought a toaster. (Please hold your applause.) The toaster is so generic it does not even have a brand name on the instructions. “Instructions,” you ask? For a toaster?

Yes, it came with a full-color, multi-step instruction, which is awesome.

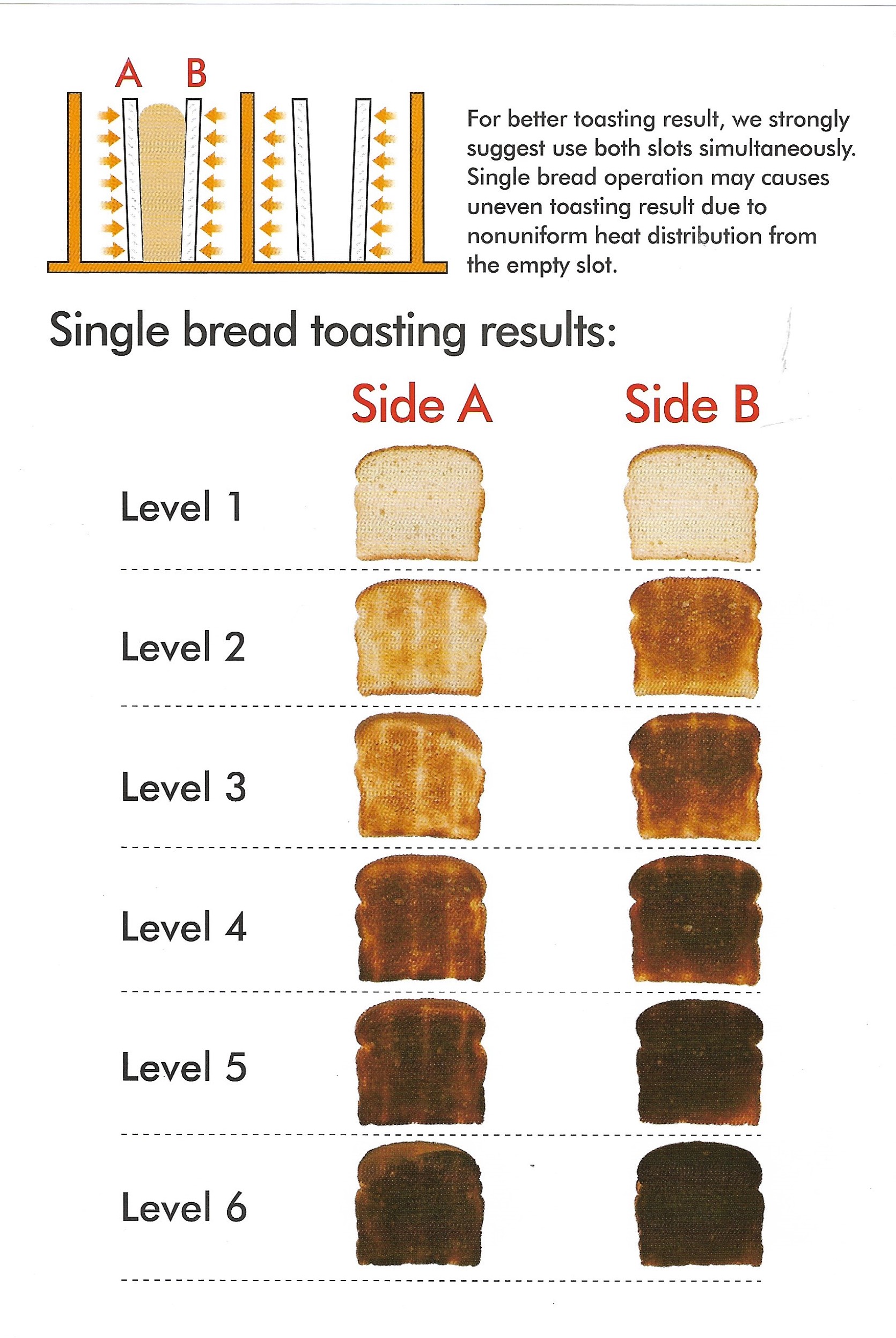

There are “Single bread toasting” instructions in case you might not want to…you know…toast two pieces of bread at the same time. And I quote, “Single bread operation may cause uneven toasting result due to nonuniform heat distribution from the empty slot.”

So, I am getting a toaster, a grammatical mistake, and entertainment all for the price of a toaster.

But wait, there’s more. It gets better! And here is the tie in with our business: It shows actual, color photographs of pieces of toast corresponding to the level dial on the toaster, ranging from level 1 (lightly toasted) to level 6 (call the fire department). So, they are asking you to compare the color photos with your toast. I love this! Examine and compare. This is risk mitigation at its finest.

Examining F&I Practices With a Clear Head

Here is a select checklist of items to consider:

So when was the last time you examined, with a clear head, your F&I practices? When was the last time you (or a trained third party) compared a checklist to a deal folder for compliance? Are your deals “warm and toasty?” Or, do you need to call the Fire Department to hose them down?

Are you using an F&I menu? If you are, terrific. If not, start right now.

o Did the customer(s) sign it?

o Were all aftermarket products offered?

o Did the customer “Accept” or “Decline” all items?

o Was the base payment disclosed on the menu without any purchased products?

Does everyone pay for your Processing Fee? Or are there inconsistencies?

Does the amount financed on the Buyer’s Order match the Retail Installment Sales Contract (RISC)?

Is there evidence the customer has received all copies of each form they signed?

If there was a trade-in and negative equity, was it appropriately disclosed according to the Truth In Lending Act?

If aftermarket products were purchased, do the product names and amounts of money correspond correctly from the enrollment agreements to the Retail Installment Sales Contract (RISC)?

On the credit application:

o It is signed by the customer(s)?

o Are there strikeovers, numbers written over other numbers, or alterations?

o If there is more than one credit application, do the numbers match?

Do the application signatures look substantially similar to all of the other signatures?

Are all the purchased F&I products sold within the dealership’s pricing cap policy? (Do you have a pricing cap policy?)

This is a partial list representing only twenty (20%) percent of the items that you should be checking.

Examining these practices will help prevent so many problems and allegations, including (but not limited to) product stuffing (quoting a payment that includes aftermarket products), discrimination, income manipulation, Suspicious Activity Reports, and fraud. Some of the items above are just the law and you are required to comply.

Why Routine Audits Matter More Than You Think

Financial institutions are required to file Suspicious Activity Reports if they believe you have submitted false information to them. It is a requirement for them, not an option.

Some of these items may be obvious, but are you actually checking? Or have you hired a third party to check?

If a regulator walked into your dealership, could you demonstrate that you perform periodic audits to check your F&I department?

Did you know that Section 8 2. of the United States Sentencing Commission considers compliance activity when judges determine the length of jail time? You must “(1) exercise due diligence to prevent and detect criminal conduct; and (2) otherwise promote an organizational culture that encourages ethical conduct and a commitment to compliance with the law.”

It is worth noting, the Consumer Financial Protection Bureau (CFPB) recently announced they are hiring additional lawyers for compliance enforcement. Click HERE to read more.

Don’t wait until smoke is rising and alarms are blaring. Implement a compliance program now or you will be a level 6 piece of toast.

The article was also published in Dealer Marketing Magazine. You can also read the article by clicking HERE.

Leave A Comment